Scope 3 is the make-or-break factor in upcoming climate disclosure. Under California’s SB 253 and the EU’s CSRD/ESRS, companies must report value-chain emissions with evidence that withstands assurance. Get it wrong and you face penalties, rework, lost access to capital, and reputational damage. Achieve accuracy through a phased, risk-based data strategy that focuses on material categories, ensures audit readiness, and drives continuous improvement in data quality year over year.

Why Scope 3 is the fulcrum?

Both SB 253 and CSRD require large companies to report their Scope 3 emissions. Under SB 253, about 5,400 California businesses with over $1 billion in revenue must begin reporting Scope 3 emissions in 2027. The CSRD goes further, asking over 50,000 EU companies to disclose detailed sustainability information, including Scope 3 emissions, starting this year.

Why? For many companies, 70–95% of total emissions fall under Scope 3, including purchased goods, logistics, use of sold products, and end-of-life. That’s why investors and regulators now focus on value-chain transparency and credible transition plans.

(GHG Protocol: Scope 3 Standard)

What SB 253 & CSRD actually require?

- SB 253 (California) — Applies to U.S. companies with >$1B revenue doing business in CA. Scope 1–2 reporting (2025 data) begins by June 30, 2026; Scope 3 (2026 data) starts in 2027. Disclosures must follow the GHG Protocol and are subject to third-party assurance, with administrative penalties up to $500k/year for non-compliance (per CARB guidance).

Source: California Air Resources Board (CARB) Climate Disclosure FAQs: https://ww2.arb.ca.gov/ - CSRD/ESRS (EU) — Requires double materiality assessment and disclosure of Scope 3 where material, with sustainability information subject to phased limited assurance that is expected to evolve toward reasonable assurance over time. It also explicitly requires value-chain coverage and the use of robust, evidence-based methodologies.

Source: EFRAG / ESRS overview: https://www.efrag.org/

What both regimes really test: defensible boundaries, documented methods, data lineage, emission-factor governance, and an assurance-ready audit trail.

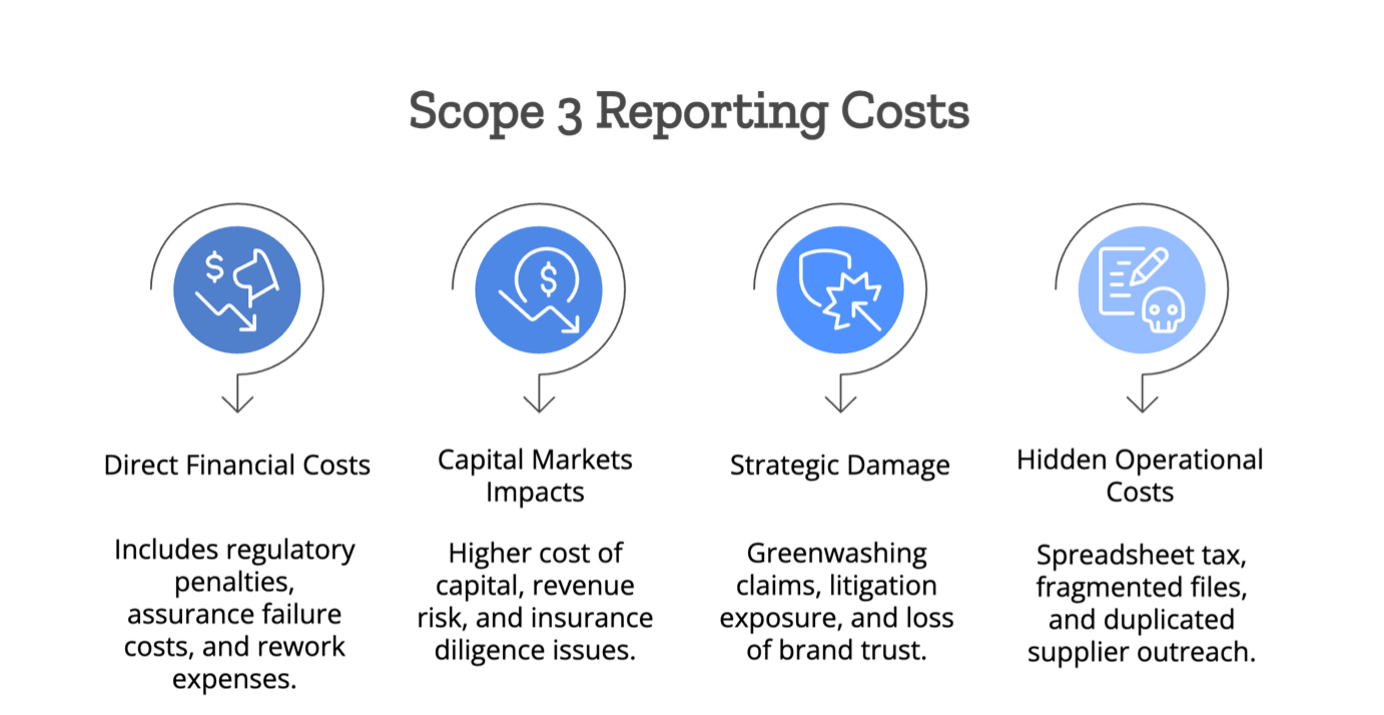

The cost of getting Scope 3 wrong

Direct financial costs

- Regulatory penalties (e.g., SB 253’s administrative penalties).

- Assurance failure costs: re-sampling, extra auditor time, delayed publication.

- Rework: re-baselining inventories, re-issuing filings, and reputation repair.

Capital markets & commercial impacts

- Higher cost of capital/exclusion from ESG-linked financing if data is unreliable.

- Revenue risk: enterprise customers increasingly require verified Scope 3 in RFPs.

- Insurance underwriters are adding climate controls to diligence.

Strategic & reputational damage

- Greenwashing claims, litigation exposure, and loss of brand trust.

Hidden operational costs

- The “spreadsheet tax”: fragmented files, outdated factors, version chaos.

- Duplicated supplier outreach across Sustainability, Procurement, and Finance.

Takeaway: It’s cheaper to design for auditability now than to fix it under scrutiny later.

Why does Scope 3 go wrong? (Common Pitfalls)

- Boundary mistakes (entity vs. operational control; double counting across scopes/categories).

- Category misclassification (e.g., Cat 1 vs. Cat 2; downstream transport vs. use phase).

- Emission-factor drift (wrong geography/year/unit; untracked updates).

- Supplier data quality (estimates without method notes; inconsistent units/periods).

- Weak controls (no maker-checker, no evidence index, undocumented assumptions).

- Over-reliance on spend-based methods where hybrid or supplier-specific is feasible.

Auditor red flags: undocumented methods, mismatched units, no tie-outs to financials, and EF sources without versions or change logs. (GHG Protocol; typical assurance guidance)

A pragmatic Scope 3 data strategy (staged, risk-based)

Design principles

- Materiality-first: attack the highest-emitting categories/suppliers.

- Evidence-backed hierarchy: supplier-specific → hybrid → spend-based (only where necessary).

- Auditability: every number must tie to source, method, owner, and period.

- Iterative uplift: improve data quality annually on a published roadmap.

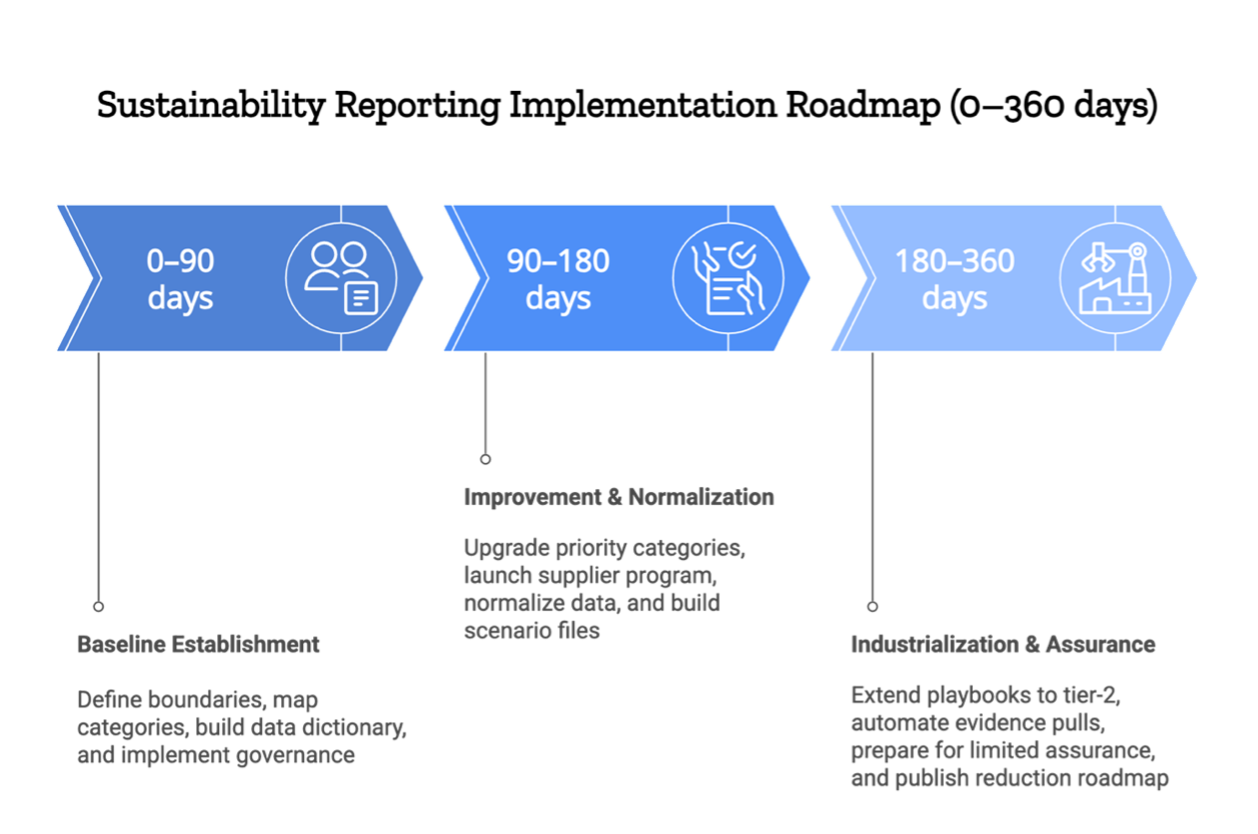

Phase 1 (0–90 days): Secure the baseline

- Confirm organisational/reporting boundaries; lock category mapping (Cat 1–15).

- Build a data dictionary (sources, owners, cadence, units) and a control matrix.

- Stand up EF governance (source hierarchy, versioning, change log).

- Implement maker-checker workflow and a central audit trail register.

- Run a hotspot heat-map to identify the top 15–20 suppliers/lanes/products by emissions.

Phase 2 (90–180 days): Improve what matters

- Upgrade priority categories to hybrid/supplier-specific methods.

- Launch a tier-1 supplier program: standard templates, cadence, and incentives.

- Normalise periods/units; add variance/outlier checks and reconcile to POs/invoices.

- Build scenario files (price/volume/EF) to quantify uncertainty and plan reductions.

Phase 3 (180–360 days): Industrialise & assure

- Extend playbooks to tier-2 via strategic tier-1s; automate evidence pulls (ERP/AP/PLM).

- Prepare for limited assurance: sampling plans, tie-outs, evidence folders, methods memos.

- Publish a reduction roadmap linking hotspots to practical decarbonization levers and capex.

Supplier data: what works?

- Segmentation: rank suppliers by volume, emission intensity, and strategic dependency.

- Data routes: standard questionnaires; utility-grade data; EPDs/PCFs where available; verified LCAs for flagship SKUs.

- Incentives: preferred status, longer terms, co-innovation; clear scorecards.

- Contractual levers: disclosure clauses, cadence, audit rights, confidentiality.

Helpful references:

- GHG Protocol Scope 3 Standard: https://ghgprotocol.org/standards/scope-3-standard

Controls, evidence & assurance readiness

- Set RACI per category owner and a monthly/quarterly close calendar.

- Enforce maker-checker validations (method, units, EF mapping, completeness).

- Reconcile to financials (GL/AP), logistics records, and production volumes.

- Manage change control: versioned methodologies; back-cast rules when EFs update.

- Prepare an assurance pack: methods memo, EF index, sampling frame, and evidence map.

Assurance expectations under CSRD and SB 253 will evolve toward stronger confidence—design your system now for that trajectory. (EFRAG; CARB)

Actionable Roadmap: Step-by-Step Compliance

- Map all possible Scope 3 categories and identify material hotspots.

- Engage priority suppliers and partners to collect high-quality GHG data.

- Select digital tools for automated data tracking and reporting.

- Clearly document all methods, calculations, and data sources.

- Conduct a gap analysis ahead of regulatory deadlines.

- Plan for annual review and improvement—Scope 3 reporting is never “done.”

Conclusion

Under SB 253 and CSRD, Scope 3 accuracy and auditability are business critical. It’s far cheaper and safer to design a materiality-first, staged data strategy now than to rebuild later under regulatory and investor pressure. Start where emissions are highest, enforce evidence and controls, improve every year, and link hotspots to real reductions. That’s how Scope 3 becomes not just compliant—but competitively valuable.

Companies that structure Scope 3 correctly from the beginning save months of rework and significantly reduce assurance costs. Credibl streamlines supplier data collection, emissions tracking, and audit documentation so sustainability and finance teams can focus on strategy, not spreadsheets.

Book a short demo to see how Credibl improves Scope 3 accuracy and audit readiness.

FAQ

1) What is Scope 3, and why is it so hard?

Scope 3 covers indirect value-chain emissions (upstream and downstream). It’s hard because data lives outside your four walls, spans many categories, and requires supplier participation and careful methods.

2) Do SB 253 and CSRD both require Scope 3?

Yes, SB 253 requires Scope 3 with phased timing and assurance. CSRD/ESRS requires Scope 3, where material and mandates double materiality and assurance. (CARB; EFRAG)

3) What level of accuracy oes auditors expect?

Auditors look for documented boundaries and methods, traceable evidence, controlled EF governance, and reconciliations to financial/logistics records. Precision improves over time, but controls and documentation are non-negotiable from day one.

4) We rely on spend-based methods. Are we at risk?

Spend-based is acceptable as a starting point, but should be prioritized for upgrade to hybrid or supplier-specific methods in material categories. Document your roadmap for uplift.

5) How do we get suppliers to share better data?

Segment suppliers, provide templates and cadence, add contractual clauses, and create incentives (preferred status, longer terms). Support with FAQs, office hours, and precise data quality rubrics.

6) What’s the quickest way to reduce Scope 3?

Target hotspots: logistics optimization, material swaps, supplier fuel-switching, product redesign. Build a MACC to prioritize measures with the best ROI and lowest implementation friction.

7) How soon do you think we should get in touch with our assurance provider?

Early. A pre-assurance review helps shape documentation, sampling, and controls, preventing costly last-minute fixes.