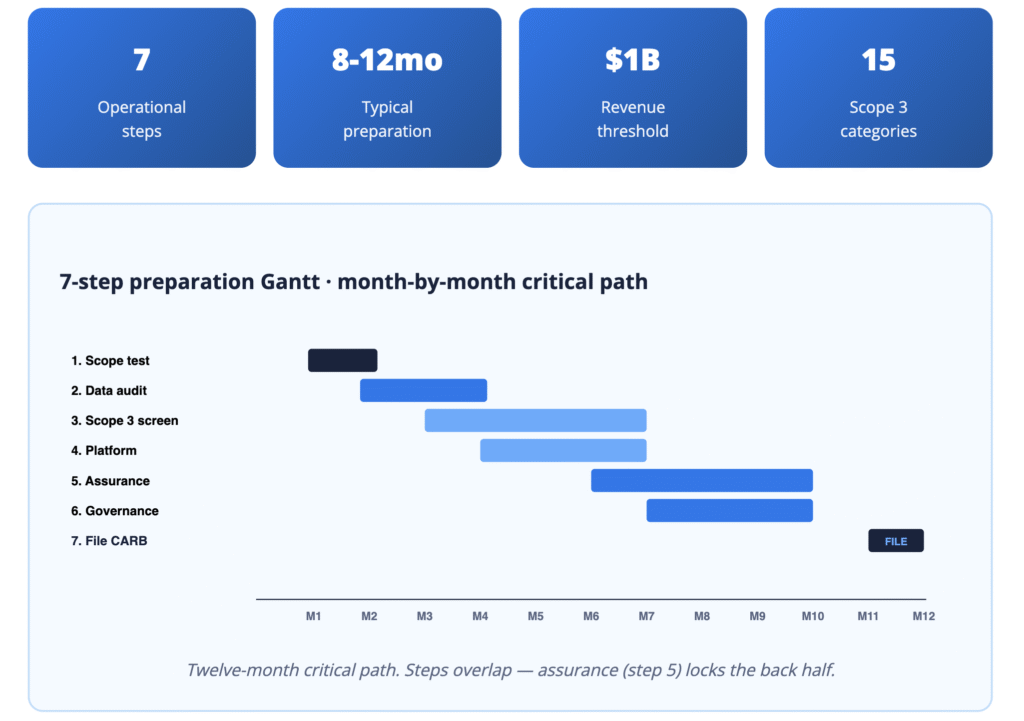

SB 253 preparation runs in seven discrete steps, from confirming scope to filing the first CARB submission. This is the operational playbook — no re-explaining the law. For the background, see the SB 253 and SB 261 ultimate guide.

Key Takeaways

- Scope confirmation hinges on consolidated worldwide revenue, not California-sourced revenue — draw a clean boundary before investing in data infrastructure.

- Scope 1 and 2 should be 80% complete before touching Scope 3 — it’s the foundation for later activity-based Scope 3 calculations.

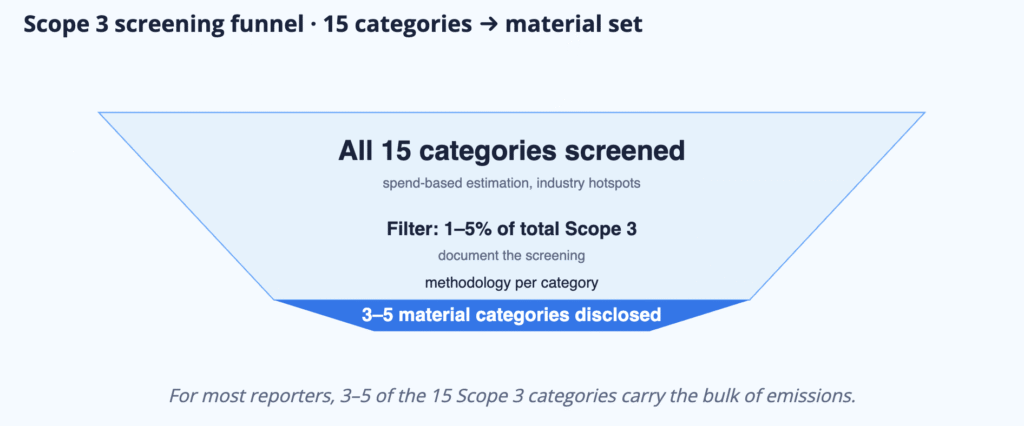

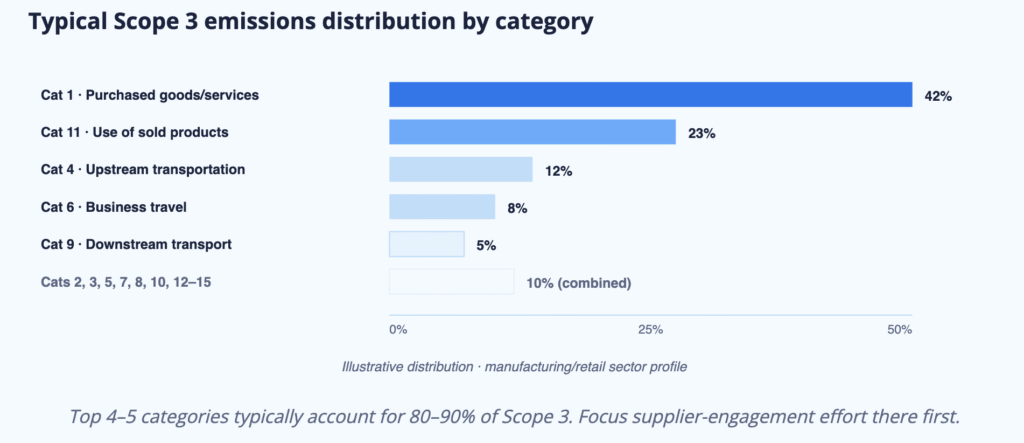

- The GHG Protocol 15-category screen, applied honestly, usually produces 3–5 material categories per company.

- Assurance-readiness is about document trails, not clever methodology — auditors want to reproduce numbers from source documents in under 30 minutes per data point.

- Internal governance (who signs off, who approves restatements) is what catches first-time reporters in year two.

Step 1 — Confirm You’re In Scope

Revenue + California nexus + entity boundary

- Pull consolidated revenue from the most recent completed fiscal year (audited financial statements — not budgets).

- Confirm California nexus: sales, employees, or tangible presence in the state.

- Map the legal entity boundary — which subsidiaries and foreign entities roll up?

- Document the revenue test annually if revenue is at or near the $1B line.

Step 2 — Audit Your Emissions Data

Inventory every emissions-relevant source

- Inventory every source — owner, cadence (monthly / quarterly / annual), and data quality (primary, spend-based, estimate).

- Confirm Scope 1+2 data: utility invoices, fuel purchases, fleet data, refrigerant logs.

- Assess Scope 3 baseline data: supplier surveys, ERP purchase records, T&E data.

- Produce a single inventory document — it drives every downstream decision.

Step 3 — Screen All 15 Scope 3 Categories

Screen, categorize, pick a method per category

- Screen all 15 GHG Protocol categories using spend-based or industry-hotspot data.

- Identify categories exceeding 1–5% of total Scope 3 as material.

- Document the screening — CARB doesn’t require disclosure of immaterial categories, but the analysis must exist.

- Assign methodology per category: spend-based for tail, hybrid for mid, supplier-specific or activity-based for top categories.

- Launch a top-20-to-50 supplier data program. Response rate under 30% in year one is normal.

Step 4 — Choose a Reporting Platform

Five non-negotiable capabilities

- GHG Protocol-aligned calculation engine with transparent, swappable emission factors.

- Scope 3 across all 15 categories with automatic method escalation.

- Audit-grade data lineage retrievable per data point.

- CARB-formatted output — not a PDF you manually restructure.

- Multi-framework mapping: one dataset → SB 253, SB 261, CDP, IFRS S2, CSRD E1.

The best SB 253 and SB 261 reporting solutions comparison gives the full evaluation matrix across eight platforms.

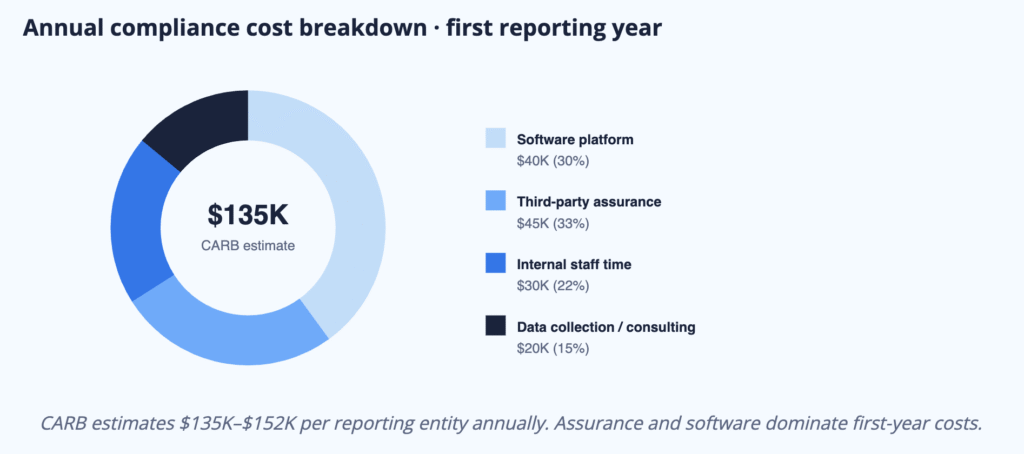

Step 5 — Plan for Third-Party Assurance

Six months out, not six weeks

- Engage an assurance provider six months before the filing window — not six weeks.

- Confirm CARB accreditation explicitly — not every Big 4 or boutique firm is or will be accredited.

- Run a pre-assurance review: walk the auditor through your data architecture, methodology, and sample data points before the formal engagement starts.

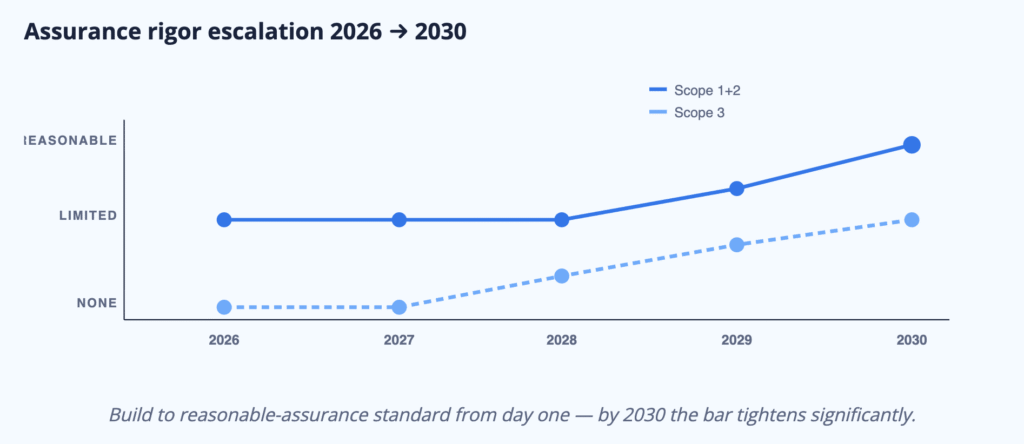

- Build to reasonable-assurance standard from day one — even though 2026 is limited assurance.

Ninety percent of assurance findings surface at the pre-engagement review, and fixing them pre-engagement is cheaper than fixing them mid-fieldwork.

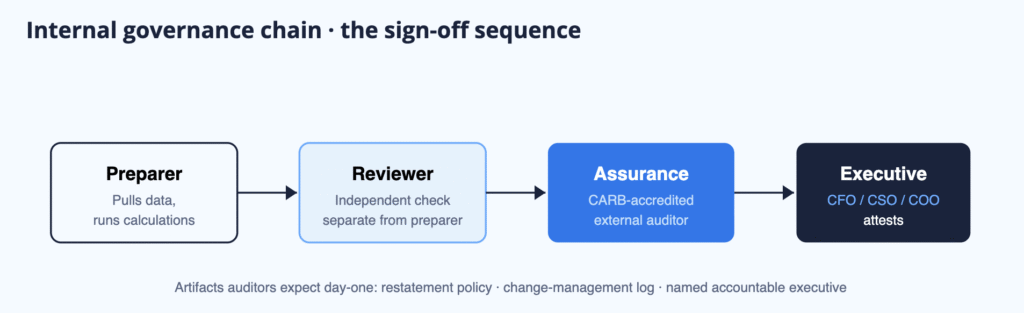

Step 6 — Set Up Internal Governance

Four artefacts auditors ask for, on day one

- Named accountable executive (CFO, CSO, or COO) who signs the attestation.

- Separate preparer and reviewer roles — the person who pulls data cannot be the signer.

- Restatement policy: trigger, approval chain, disclosure pattern.

- Change-management log for emission-factor, methodology, and boundary changes.

Step 7 — File With CARB

Internal review → assurance sign-off → attestation → submit

- Internal review by finance, legal, and sustainability leads.

- Assurance sign-off on the emissions dataset.

- Executive attestation.

- Submit to CARB through the digital platform during the open filing window (first: August 10, 2026).

- Monitor CARB’s public registry and handle post-submission restatements per policy.

⚠ Five Mistakes That Cost Year-One Programs

- Treating Scope 3 as optional in year one — infrastructure built in 2026 or not at all.

- Building a custom spreadsheet “solution” that can’t produce CARB-format output without manual rework.

- Using an assurance provider that isn’t CARB-accredited.

- Failing to document the in-scope revenue test — year-three defense depends on the trail from year one.

- Confusing SB 261 climate-risk disclosure with SB 253 emissions disclosure — different cadence, different penalty, different filing destination.

Frequently Asked Questions

1. How long does SB 253 preparation take?

Eight to twelve months is typical for a company starting from spreadsheet-based tracking. Companies with mature CDP programs can compress to four to six months.

2. Can we outsource SB 253 compliance entirely?

The reporting platform can be outsourced; the accountability cannot. CARB expects the reporting entity’s executives to attest. Assurance providers audit the company’s data, not a consultant’s work product.

3. What if we can’t get Scope 3 data from suppliers?

Use spend-based estimation in year one, document the data gap, and show a plan to close it. Auditors accept documented gaps that are being actively addressed; they reject undisclosed gaps.

4. Can one reporting platform handle SB 253, SB 261, CDP, and CSRD?

Yes, if the platform uses a unified data model. Credibl maps one set of emissions data to all four framework outputs.

5. Do intra-group transactions need to be eliminated for SB 253?

Yes. The GHG Protocol consolidation rules apply — intra-group Scope 1 and 2 emissions are netted within the consolidated reporting boundary.