Introduction

As sustainability reporting becomes more standardized and globally enforced, companies are being asked to navigate different, and sometimes overlapping, ESG frameworks. Two of the most influential right now are the EU’s CSRD (Corporate Sustainability Reporting Directive) and the ISSB’s IFRS Sustainability Disclosure Standards.

A key difference between them? Their definition of materiality.

While the ISSB employs a single materiality approach, focusing solely on how sustainability affects a company’s financial performance, the CSRD adopts a double materiality approach, which also considers how a company impacts people and the planet.

This blog explains what each approach means, how they influence reporting, and how sustainability teams can reconcile both perspectives in a single, unified workflow.

What Is Materiality in ESG Reporting?

In ESG, materiality refers to what’s important enough to disclose. But important to whom? And in what context?

- Single materiality (used by ISSB): Focuses on how sustainability issues affect the company’s financial performance. If a risk or opportunity could influence investor decisions, it’s considered material.

- Double materiality (used by CSRD): Includes the above and how the company’s operations impact the environment and society. So even if an issue isn’t financially material, it’s still reportable if it has a significant external impact (e.g. biodiversity loss or human rights violations).

In other words, CSRD requires companies to think both inside-out and outside-in, whereas ISSB is primarily concerned with the outside-in financial view.

Why These Definitions Matter

Materiality shapes everything , from what data you collect to what you report publicly.

- Under ISSB, your audience is investors and capital markets. The aim is to provide decision-useful information on the company’s ability to generate value.

- Under CSRD, your audience also includes regulators, civil society, employees, customers, and communities. The aim is transparency , even if a topic isn’t yet financially material.

Each approach reflects a different philosophy. The ISSB sets a global baseline for investor-grade disclosures, while the CSRD adds stakeholder accountability through impact reporting.

Regulatory Scope: Who Reports What?

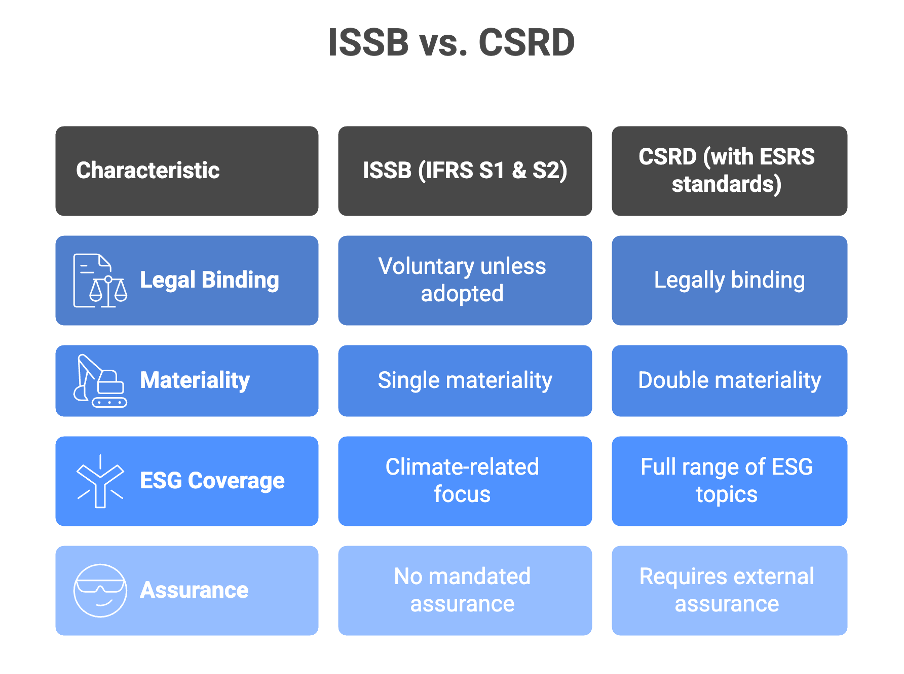

ISSB (IFRS S1 & S2)

- Voluntary unless adopted by national regulators (e.g. UK, Singapore, Canada may align soon).

- Based on single materiality (enterprise value).

- Focus is currently on climate-related disclosures (IFRS S2), with other ESG topics expected to follow.

- No mandated assurance (unless required by local laws).

CSRD (with ESRS standards)

- Legally binding for all large companies and listed SMEs operating in the EU (and some non-EU companies with significant EU business).

- Based on double materiality.

- Covers the full range of ESG topics under the European Sustainability Reporting Standards (ESRS).

- Requires external assurance of sustainability disclosures.

In practice, many global companies, especially multinationals, will need to comply with both frameworks.

Strategic Impact: Two Lenses, One Strategy

While CSRD and ISSB differ in their materiality definitions, they don’t need to conflict. In fact, companies can and should use both perspectives to inform a more resilient ESG strategy.

- Single materiality helps protect financial value: Think of it as traditional risk management applied to sustainability.

- Double materiality helps protect long-term legitimacy: It captures reputational, social, and environmental factors that may not be financial today but could become critical tomorrow.

Combining both gives companies a more holistic picture of risk, opportunity, and responsibility, aligning shareholder value with stakeholder trust.

Materiality Assessments: The Foundation of Both

Whether you’re reporting under CSRD, ISSB, or both, the process begins with a materiality assessment.

- For CSRD, you must assess both impact materiality and financial materiality.

- For ISSB, only financial materiality is required, but the evaluation should still be rigorous and evidence-based.

Many companies are now running one combined assessment that serves both purposes. This means evaluating:

- How do ESG issues affect your company’s financial performance?

- How do your company’s activities affect people and the planet?

The overlap can then be used to streamline reporting for both frameworks.

One Workflow, Two Outputs: Practical Integration Tips

Here’s how to reconcile CSRD and ISSB in a single ESG reporting process:

- Start Broad, Narrow Later

Begin with a double materiality assessment. It will capture both financial and impact topics. From there, extract the subset of issues that meet single materiality thresholds for ISSB disclosures.

- Map Requirements

Use a crosswalk to align ESRS (CSRD) topics with ISSB’s IFRS S1 and S2. Many core disclosures, especially climate-related, overlap.

- Collect Once, Report Twice

Use the same ESG data infrastructure and processes to serve both reporting needs. One platform, multiple outputs.

- Harmonize Language and Governance

Build one consistent narrative around the sustainability strategy that works across both disclosures. Governance, risk management, and KPIs should tell the same story, even if the audiences differ.

- Enable Future-Proofing

Adopting double materiality today prepares you for future regulatory changes. What isn’t financially material now may become so in the years ahead.

Conclusion: Streamlining Global ESG Reporting Starts Here

Reconciling CSRD’s double materiality and ISSB’s single materiality doesn’t require two teams or two reports. With a smart, integrated workflow, companies can meet both obligations while building a strategy that is resilient, transparent, and future-ready.

At Credibl, we help sustainability teams unify their materiality assessments, align with both the CSRD and ISSB standards, and manage disclosures from a single intuitive platform. Whether you’re navigating EU compliance or preparing for investor scrutiny, our ESG data and reporting solution is built for global complexity and audit-ready clarity.

Book a demo with Credibl to simplify your ESG workflows and stay ahead of evolving standards: crediblesg.com

FAQs

Q1: Can I comply with ISSB by doing a CSRD double materiality assessment?

Yes, a well-executed double materiality assessment will cover financial materiality too. You can use it to satisfy ISSB’s single materiality requirements with minimal additional work.

Q2: Do I need to create two separate reports?

Not necessarily. Many companies opt to publish a single integrated sustainability report, accompanied by cross-references or appendices that provide ISSB/CSRD-specific content.

Q3: How often should we update our materiality assessment?

Best practice is to update at least every 2–3 years, or sooner if there are major business, stakeholder, or regulatory changes.

Q4: Does double materiality mean reporting on everything?

No, it means disclosing issues that are either financially material or have a significant environmental or social impact. There’s still a threshold for relevance.

Q5: Is ISSB really “just for investors”?

Primarily, yes. But many stakeholders benefit from investor-grade data, and over time, non-investor audiences (regulators, customers, employees) may demand alignment too.