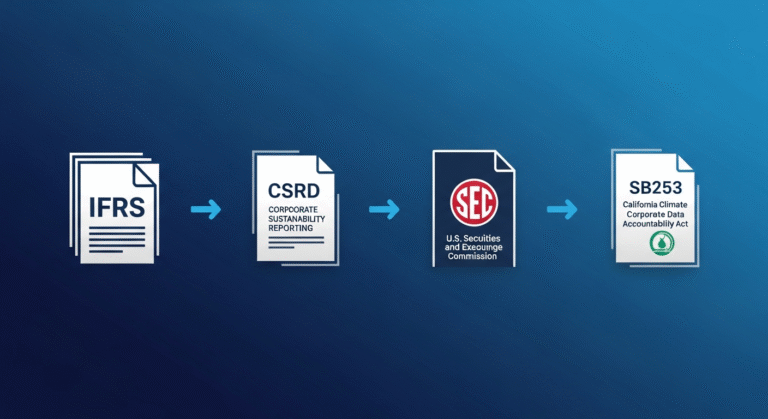

Multinationals face up to four overlapping climate disclosure regimes — IFRS S1/S2 (global via ISSB), EU CSRD, the US SEC climate rule, and California SB 253. The legal requirements differ; the underlying emissions data does not. This page compares the frameworks and shows how to run one emissions program that feeds all four.

Key Takeaways

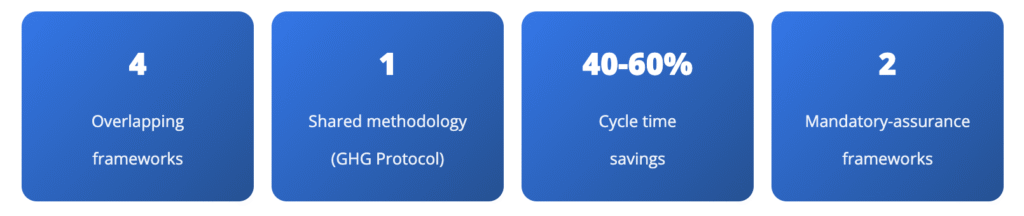

- IFRS S1/S2, CSRD, SEC, and SB 253 all lean on the GHG Protocol for emissions calculation — the same underlying data supports every filing if infrastructure is designed that way.

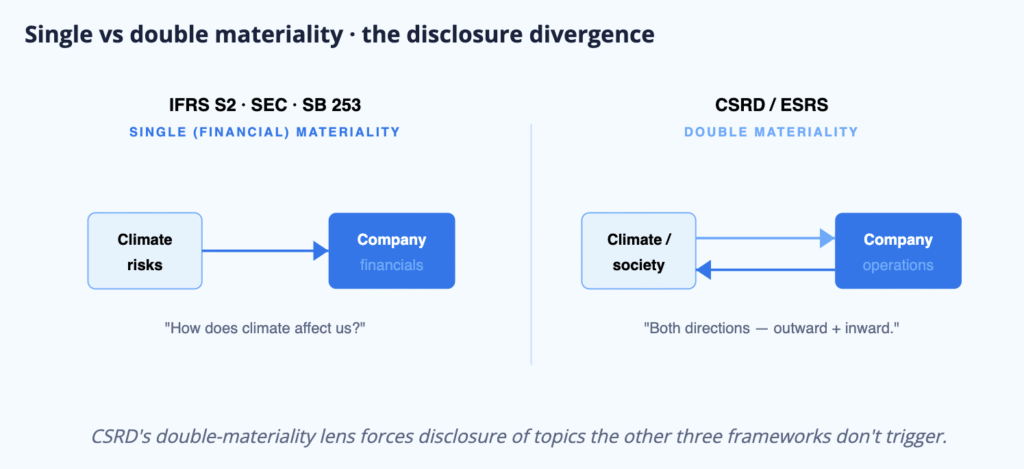

- CSRD is the broadest in scope (double materiality across E, S, and G); SB 253 is the narrowest (emissions only); IFRS S2 sits in between.

- The SEC climate rule’s status has shifted during 2024–2026 — its applicability is the most uncertain of the four; SB 253 is stable.

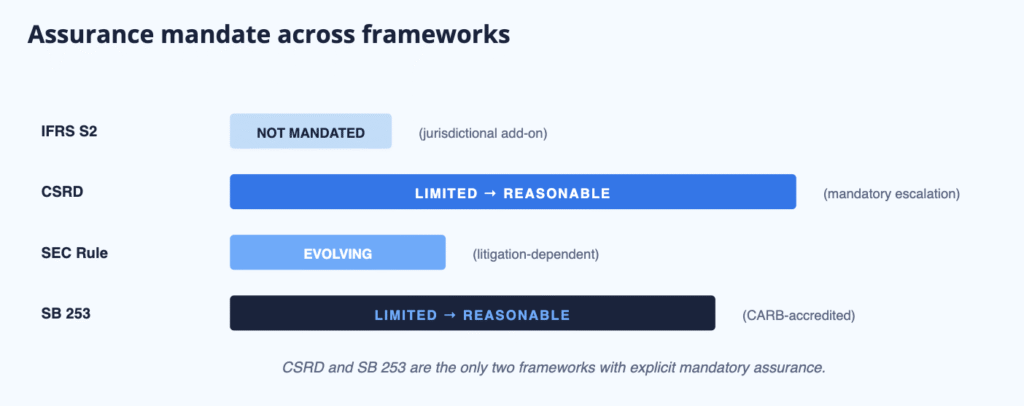

- Assurance requirements diverge: CSRD mandates limited assurance on all disclosures; SB 253 mandates assurance on emissions; IFRS S2 requires none by default.

- Report-once-map-to-many infrastructure cuts multi-framework reporting time by 40–60% versus running each program separately.

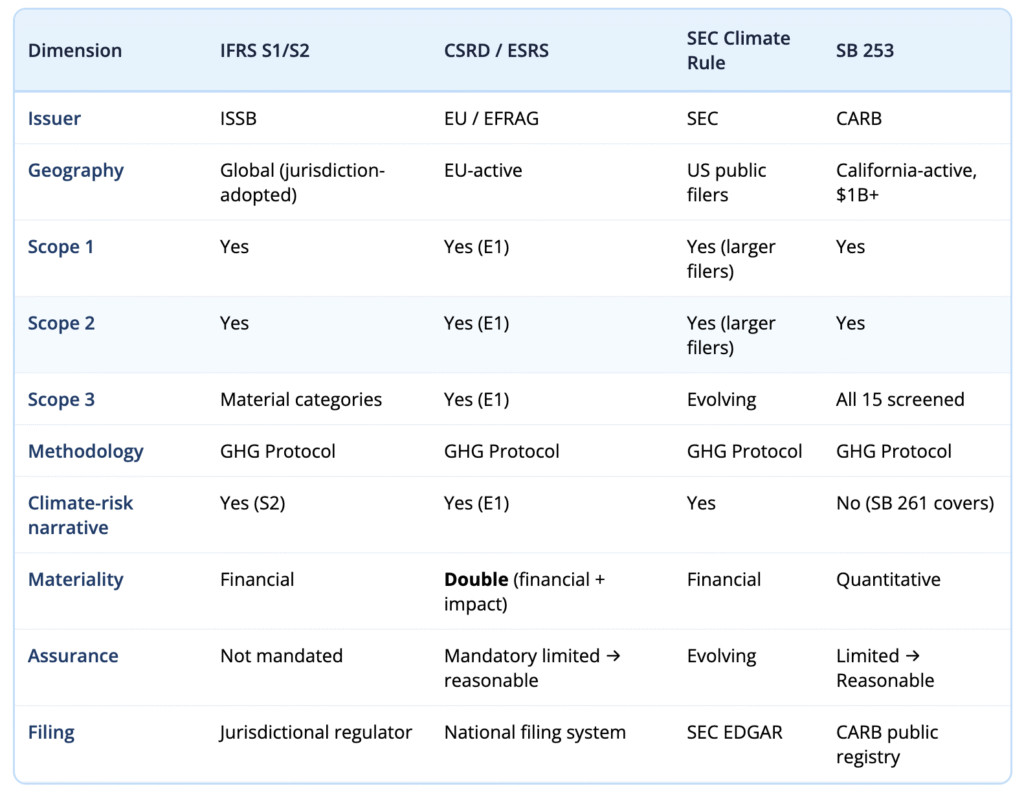

Full Side-by-Side Comparison

The Four Frameworks Multinationals Are Tracking

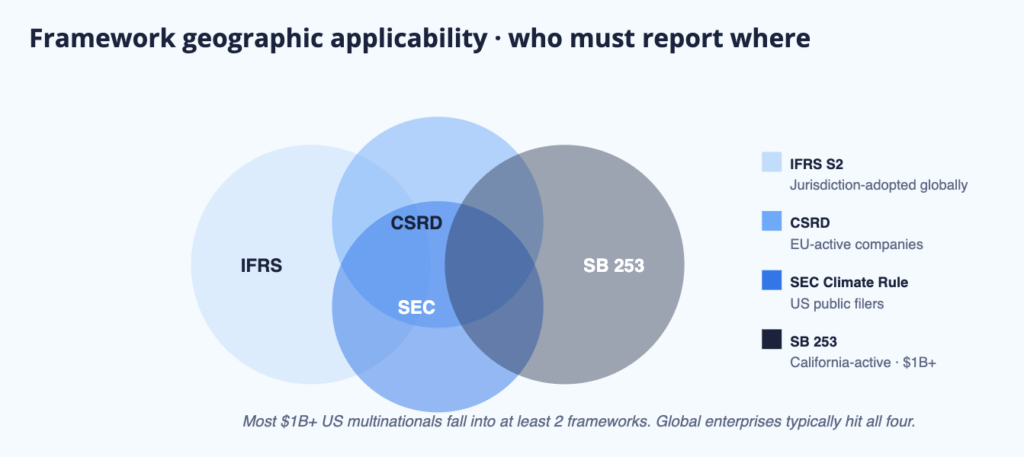

IFRS S1 and S2

ISSB · Global, adopted jurisdiction-by-jurisdiction

Global sustainability disclosure standards issued by the ISSB. S1 covers sustainability-related financial information broadly; S2 is climate-specific. Voluntary globally, but individual jurisdictions (UK, Australia, Canada, Hong Kong, Brazil, others) are adopting them as mandatory regimes.

EU CSRD / ESRS

EU · Mandatory for EU-active companies, double materiality

The Corporate Sustainability Reporting Directive, implemented through the European Sustainability Reporting Standards. Mandatory for large EU-active companies and covers environmental, social, and governance disclosures under a double-materiality framework.

SEC Climate Disclosure Rule

SEC · US federal, status uncertain

The US federal rule issued in 2024. Its scope and enforcement have evolved through litigation and regulatory review. Current practical advice: monitor SEC rule making bulletins, build emissions infrastructure under the GHG Protocol regardless, and treat SEC as a floor, not a ceiling.

California SB 253

CARB · California-active, $1B+ revenue

State-level mandatory disclosure of Scope 1, 2, and 3 emissions for companies above $1B revenue doing business in California. The SB 253 and SB 261 ultimate guide covers requirements and deadlines.

Where the Frameworks Overlap

The foundation is the same:

- GHG Protocol emissions methodology — Scope 1, 2, 3 calculations are portable across all four frameworks.

- Scope 3 category-by-category disclosure — IFRS S2, CSRD E1, and SB 253 all use the 15-category structure.

- Third-party assurance — CSRD and SB 253 explicitly mandate it; IFRS S2 and SEC frequently require it at the jurisdictional level.

- Audit-trail expectations — every framework expects reproducible calculations back to source documents.

Where the Frameworks Conflict

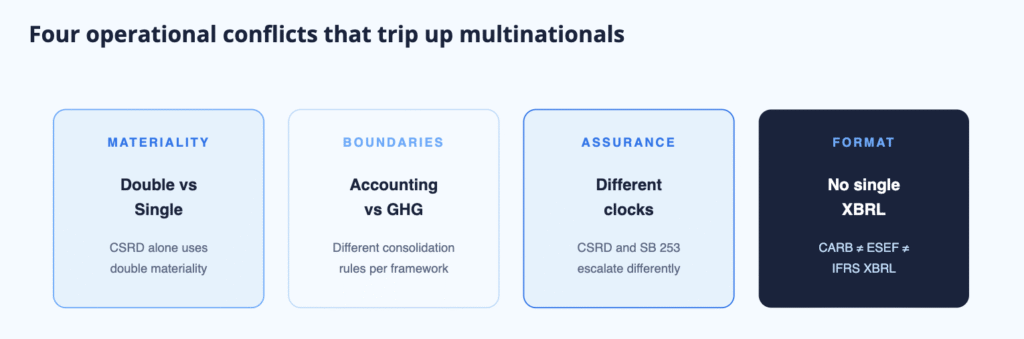

The operational differences that trip up multinationals:

- Materiality definition. CSRD’s double materiality (financial + impact) is not how IFRS S2, SEC, or SB 253 define materiality. Disclosures under CSRD will include topics that do not appear under the other three.

- Reporting boundaries. CSRD aligns with financial accounting boundaries; SB 253 uses GHG Protocol consolidation. Most companies align them to simplify, but they can differ.

- Assurance timing. CSRD’s assurance escalation runs on a different clock than SB 253’s. Companies subject to both need to synchronize internal audit-readiness calendars.

- Disclosure format. CARB’s structured format is not CSRD’s ESEF/XBRL format, which is not ISSB’s IFRS XBRL. The same emissions number must be re-packaged for each filing.

Citation Capsule: The GHG Protocol Corporate Standard underpins all four frameworks’ emissions methodology. Companies that build around this data model — rather than any single framework’s template — reduce duplication by 40–60% in year two (Credibl customer benchmarking, 2025).

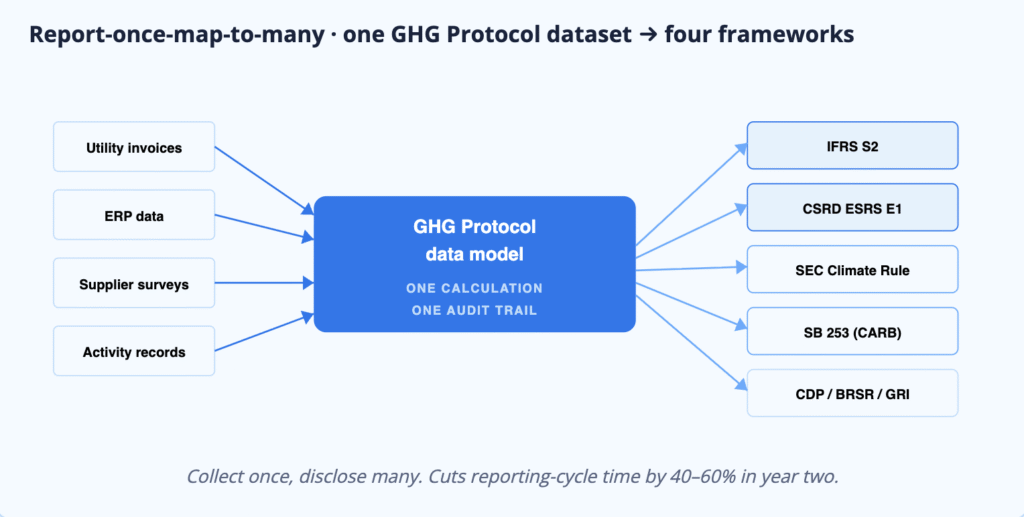

How to Report Once, Map to Many

Build the infrastructure around the GHG Protocol data model, not around any one framework’s disclosure template. The operational pattern:

- One emissions calculation engine — Scope 1, 2, 3 under GHG Protocol.

- One data-collection workflow — utility invoices, ERP purchase data, supplier questionnaires, activity records.

- One audit trail — timestamped per data point, retrievable to source documents.

- Multiple framework outputs — the same dataset produces CSRD ESRS E1, IFRS S2, SEC climate, SB 253, CDP.

- One assurance engagement where possible — CSRD and SB 253 assurance providers can often audit the underlying dataset once, then attest separately to each framework’s presentation.

Companies that build this infrastructure cut reporting-cycle time by 40–60% in year two versus running each framework as a separate program.

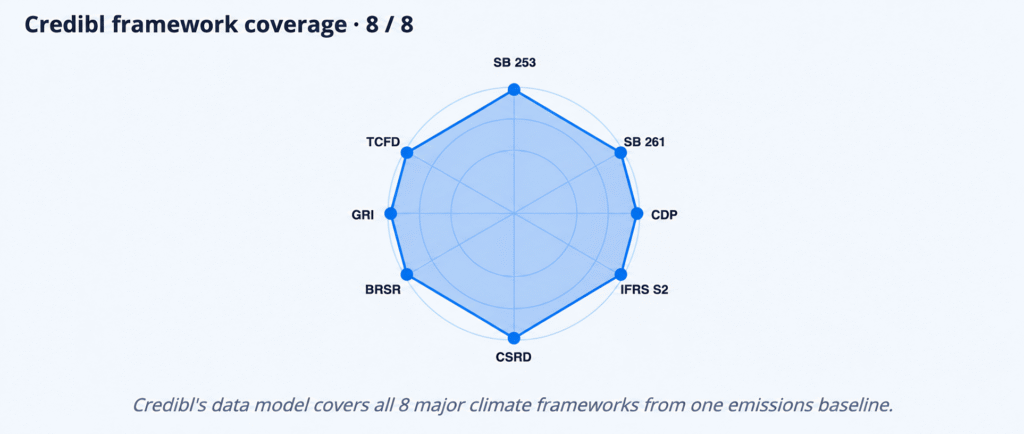

How Credibl Handles Multi-Framework Reporting

Credibl runs a GHG Protocol-aligned data model that feeds SB 253, SB 261, CSRD ESRS E1, IFRS S2, CDP, BRSR, GRI, and TCFD outputs from the same emissions baseline. The platform:

- Collects Scope 1, 2, and 3 data once

- Maps resulting emissions to each framework’s disclosure template automatically

- Produces a single audit trail that assurance providers can verify across all filings

- Updates framework-specific outputs when ESRS, ISSB, or CARB templates change — without requiring data re-entry

Multi-framework reporters typically compress their reporting calendar by three to four months annually after the first full cycle.

Frequently Asked Questions

Does IFRS S2 compliance satisfy SB 253?

Not automatically. IFRS S2 uses the same GHG Protocol methodology, but SB 253 requires CARB-formatted filing and CARB-accredited assurance.

If we comply with CSRD, do we need SB 253 disclosures too?

Yes, if you exceed the SB 253 threshold ($1B revenue) and do business in California. CSRD is EU law; SB 253 is California law. Compliance under one does not remove obligations under the other.

Which framework is the hardest?

CSRD, because of double materiality and the breadth of E, S, and G topical standards. SB 253 is narrower but introduces the first mandatory Scope 3 regime in the US.

Can one assurance provider audit all our disclosures?

Often yes. Audit firms accredited for multiple frameworks (Big 4 and major assurance providers) can cover CSRD, IFRS S2, SB 253, and SEC within a single engagement, provided data lineage supports it.

What changes if the SEC rule is delayed further?

Companies still have SB 253, IFRS S2 (where adopted), and CSRD obligations. The SEC rule’s status doesn’t change state or international requirements.