At first glance, Business Responsibility and Sustainability Reporting (BRSR) can seem like a simple disclosure requirement.

In reality, it feels more like assembling a cricket team where everyone shows up with talent, but no one is quite sure who’s bringing the bat, who’s keeping score, or who’s actually bowling.

That lack of clarity is exactly where most BRSR reporting challenges begin. It is rarely a question of willingness. ESG data collection sits across departments, suppliers respond at their own pace, and reporting processes are often stitched together through spreadsheets, emails, and last-minute follow-ups.

As SEBI gradually tightens BRSR Core assessment and assurance requirements for the top 1,000 listed companies in India, (while value-chain disclosures continue to evolve separately), the focus is no longer on reporting “something”. It is on reporting something reliable.

| Issue | What it looks like in practice | Why it happens | How to possibly respond |

| Inconsistent ESG data from multiple teams | Same metric reported with different periods, units, methods; multiple “final_final” files in circulation | Ownership is diffused; no common definitions or data standards across departments | Assign one owner per material metric and standardise definition, frequency, and required evidence early |

| Scope 3 data incomplete, delayed, unreliable | Missing supplier data, mixed methodologies, late responses; fallback to spend‑based estimates at deadline | Supplier ESG maturity varies; questionnaires are low priority versus BAU work | Start with most material categories and top suppliers, use estimates transparently, and improve data quality year‑on‑year |

| Materiality and disclosure priorities unclear | Teams unsure what to detail, what to evidence, and what is truly “material”; everything feels urgent | Materiality treated as a workshop slide, not as an input to data, ownership, and reporting depth | Turn material topics into concrete workflows: assign owners, timelines, and evidence expectations for each material topic |

| Spreadsheet heavy, hard‑to‑audit reporting | Version confusion, broken formulas, copied tabs, manual overrides, no trace back to source documents | Data lives across ERPs, HRMS, procurement, PDFs, emails; consolidation is manual and late | Move from collection to control: templates, deadlines, version history, stored evidence, and early anomaly review |

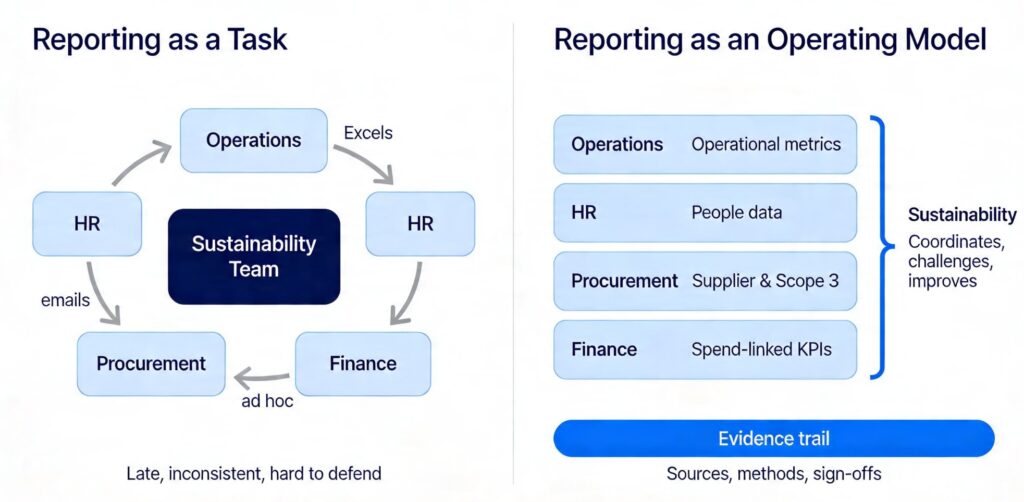

| BRSR ownership sits with one team, not business | Sustainability team is expected to “do everything” without controlling underlying data | BRSR seen as a reporting task, not an operating model; functions don’t own “their” metrics | Make BRSR cross‑functional: Ops/HR/Procurement/Finance own data; Sustainability coordinates, challenges, and improves |

| Preparation for submission, not assurance | Focus on filling the form; limited ability to explain or defend numbers when challenged | Submission has a hard deadline; assurance readiness feels like a future problem | Build evidence discipline early: keep sources, methods, assumptions, and sign‑offs for any metric important enough to publish |

Why BRSR Reporting Feels Harder Than It Looks

A BRSR report is rarely built by one team.

- Operations has energy and waste data

- HR has diversity and training data

- Procurement has supplier information

- Finance has spend

- Legal has policies

Sustainability is expected to pull it all together and make it audit-ready.

That is why ESG reporting challenges India are often less about intent and more about coordination.

Everybody is busy, everyone has partial data, and by the time it all arrives, it kind of resembles a family WhatsApp thread during wedding season: lots of activity and confusion but no clear direction!

Here’s how these challenges typically show up in practice:

1. Inconsistent ESG Data Across Departments: A Core BRSR Data Management Problem

One of the most common ESG data issues in BRSR reporting is simple inconsistency.

One plant reports monthly power consumption. Another sends annual totals. One team uses invoices. Another uses estimates.

Someone updates a spreadsheet. Someone else uses last year’s format. Now the numbers do not tie up, and everyone suddenly is very interested in whose sheet is the “final final” file.

Why this happens

Because data ownership is often spread across departments, but data standards are not.

Most organisations start with good intentions and a shared folder. Unfortunately, a shared folder is not the same thing as a reporting system.

How to solve it

Start by assigning one owner for each material metric. Not one team for ten metrics. One owner per metric.

Then standardise three things early:

- The definition of the metric

- The reporting frequency

- The evidence required to support it

This sounds basic because it is basic. But basic is exactly what prevents year-end chaos.

Many sustainability reporting problems are not strategic failures. They are process failures wearing a serious face.

2. Scope 3 Data Is Incomplete, Delayed, Or Unreliable

If Scope 1 and 2 are difficult, Scope 3 has a special talent for humbling even well-prepared teams.

Supplier data may be missing. Methodologies may vary. Some vendors may not track emissions at all. Others may send partial data in different formats.

And when the deadline gets closer, teams often fall back on spend-based estimates simply because there is no other practical option.

These are classic Scope 3 data challenges, and they are especially relevant in large supply chains where data maturity differs widely across vendors.

Why this happens

Because your reporting maturity is only as strong as the weakest data link in the value chain.

Also, suppliers have their own priorities. Your ESG questionnaire may not be sitting at the top of their to-do list between dispatch schedules, payment follow-ups, and quarter-end reviews.

How to solve it

Start with the most material categories and the most important suppliers. Build a phased approach:

- Use estimates where necessary

- Focus on top suppliers by spend or impact

- Improve supplier-specific data over time

- Document assumptions clearly

The goal is not perfection on day one. The goal is a method that gets better every year.

This is also where technology can help. For large enterprises and financial institutions, a platform like Credibl helps reduce data fragmentation by centralising ESG inputs, pulling from structured and unstructured documents, and supporting supplier assessment, benchmarking, and assurance-ready workflows.

3. Materiality And Disclosure Priorities Are Unclear

Another major source of BRSR implementation problems is not knowing what deserves the most attention.

Teams often ask:

- What must we disclose in detail?

- Which metrics need tighter evidence?

- Which topics are actually material to our business?

Without clear priorities, reporting becomes reactive. Everything looks urgent, so nothing gets handled properly.

Why this happens

Because materiality is sometimes treated as a workshop exercise instead of a business decision.

If the materiality process sits in a presentation deck and never influences data collection, ownership, or reporting depth, it will not help much when reporting season starts.

How to solve it

Keep materiality practical.

Identify the topics that matter most to the business, stakeholders, and regulatory disclosures. Then connect those topics directly to reporting workflows.

If water, waste, labour practices, or supplier conduct are material, make sure those metrics have owners, timelines, and evidence expectations attached to them.

4. Reporting Is Still Spreadsheet-Heavy and Hard to Audit

Spreadsheets are useful. They are also responsible for many headaches in BRSR reporting.

The problem is not the spreadsheet itself. The problem is what happens around it: version confusion, broken formulas, copied tabs, manual overrides, missing comments, and no audit trail. It works until it does not.

Why this happens

Because sustainability data often lives across ERP systems, HRMS platforms, procurement tools, utility portals, PDFs, emails, and plant-level registers.

Pulling all of that into one consistent view manually takes time and invites error.

How to solve it

Move from collection to control.

Even if you are not using a full-scale platform yet, create a more disciplined workflow:

- Use standard templates

- Define submission dates

- Store evidence with the metric

- Keep version history

- Review anomalies early

This is where AI-backed ESG solutions like Credibl become far more useful. Instead of treating ESG as a manual consolidation exercise, the platform automates data collection across sources, standardises inputs, flags anomalies through AI-driven variance checks, and maintains a clear, auditable trail across frameworks.

Because the real win is not speed. It is being able to answer, without hesitation: “Can you show me where this number came from?”

5. BRSR Ownership Sits with One Team Instead of The Business

A common issue in ESG reporting challenges India is that sustainability teams are expected to own everything, even when they control very little of the source data.

That is a tough arrangement. It is a bit like making one person host the meeting, take notes, prepare the deck, and also answer all the technical questions.

Admirable, but not scalable.

Why this happens

Because BRSR is still seen in some organisations as a reporting task rather than an operating model.

When that happens, sustainability becomes the department that chases data instead of the function that drives performance.

How to solve it

Treat BRSR as a cross-functional programme.

Operations should own operational metrics. HR should own people data. Procurement should own supplier engagement. Finance should validate spend-linked numbers. Legal and compliance should review policy-linked disclosures.

Sustainability should coordinate, challenge, and improve the process, not act as a one-man collection agency.

6. Companies Prepare for Submission, Not Assurance Readiness

This is one of the most underestimated BRSR challenges.

Many teams focus on completing the report. Fewer focus on whether the numbers can be explained, traced, and supported.

That is a problem, especially as BRSR Core assessment or assurance expectations continue to expand for larger listed entities.

Why this happens

Because submission has a visible deadline. Assurance readiness feels like a future problem.

How to solve it

Build “evidence discipline” early.

For key metrics, keep:

- Source files

- Calculation logic

- Assumptions

- Methodology notes

- Reviewer signoffs

Do not wait until the reporting season to discover that a number was based on an estimate nobody documented six months ago.

A good rule of thumb is this: if a metric matters enough to publish, it matters enough also be defended.

A Simpler Way to Make BRSR Reporting Easier

Most sustainability reporting problems are not caused by a lack of intent. They usually come down to three things: unclear ownership, fragile data processes, and patchy evidence.

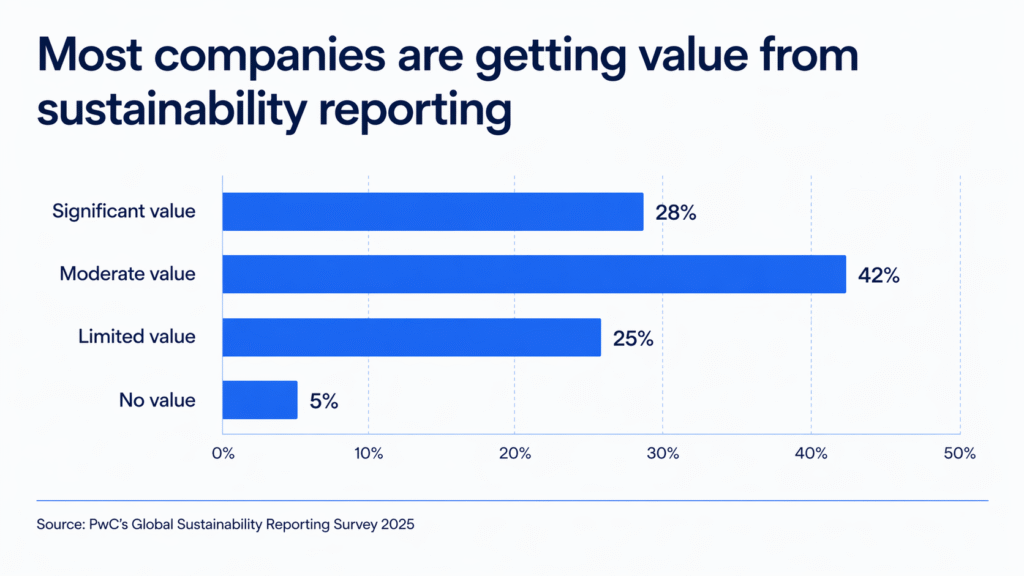

And that gap does more than create compliance risk. It also reduces the business value companies can get from ESG data. PwC’s 2025 Global Sustainability Reporting Survey found that more than two-thirds of companies already reporting under CSRD or ISSB saw significant value beyond compliance from the data and insights they collected.

That is an important shift. Because strong ESG reporting is no longer just about disclosure. Done well, it can help companies spot operational inefficiencies, improve supplier visibility, strengthen risk management, and make better long-term decisions.

In that sense, BRSR is not just a reporting requirement. It is also a management discipline.

The catch is that many organisations still approach it like a year-end school project: a burst of effort, a rush for missing inputs, and a polite hope that everything comes together in time.

That may get the report out the door, but it does very little to build a system that is repeatable, reliable, or ready for scrutiny. So the smartest way to make BRSR reporting easier is also the most practical.

Give every metric a clear owner, so responsibility sits with the person closest to the data. Start with the disclosures and suppliers that matter most, instead of trying to solve every gap in one go.

And build an evidence trail before anyone asks for it, so numbers can be explained, traced, and defended without the annual panic.

Final thoughts

Most BRSR reporting challenges and implementation problems are solvable.

Better reporting rarely comes from heroic last-minute effort. It comes from better systems, clearer accountability, and fewer moving parts. Or, to put it simply: less jugaad, more structure.

That is usually the difference between a report that looks polished and a reporting process that actually works.

FAQs

1. What are the most common BRSR reporting challenges in India?

The most common BRSR reporting challenges include inconsistent ESG data across departments, incomplete Scope 3 data, unclear materiality priorities, spreadsheet-heavy workflows with no audit trail, and lack of assurance readiness. Most of these problems trace back to the same root cause: sustainability data is owned by everyone and controlled by no one.

2. Why is ESG data collection difficult for BRSR reporting?

BRSR data sits across operations, HR, procurement, finance, legal, and suppliers — each with different systems, formats, and timelines. Without standardised definitions, assigned owners, and documented evidence requirements, companies end up with multiple versions of the same metric and no clear way to reconcile them before submission.

3. How can companies solve inconsistent ESG data in BRSR?

Assign one owner per material metric — not one team for ten metrics. Then standardise three things early: the definition of the metric, the reporting frequency, and the evidence required to support it. Most ESG data inconsistency is a process failure, not a data failure.

4. Why is Scope 3 data a challenge in BRSR reporting?

Scope 3 data depends on suppliers, many of whom have limited ESG maturity or treat questionnaires as low priority. The practical fix is to start with your most material categories and top suppliers by spend, use estimates transparently where data is missing, and improve supplier-specific data quality year on year.

5. How can companies prepare for BRSR Core assurance?

Start building evidence discipline before reporting season. For every key metric, maintain source files, calculation logic, assumptions, methodology notes, and reviewer sign-offs. SEBI’s BRSR Core framework is tightening assurance expectations for large listed entities — if a number is worth publishing, it needs to be defensible.