Over the past decade, sustainability in Europe has evolved rapidly. What began as voluntary corporate responsibility initiatives has now become a core component of financial regulation, industrial policy, and capital markets.

Recent developments across Europe illustrate a clear shift. Climate risks are increasingly influencing sovereign borrowing costs. Industrial policy is being designed around low-carbon competitiveness. Financial regulators are requiring sustainability preferences to be embedded into investment advice.

Individually, these developments may appear disconnected. Taken together, they reveal something far more significant: sustainability data is becoming foundational to how the European economy allocates capital, manages risk, and builds industrial competitiveness.

For companies operating in Europe, the implication is clear. Sustainability is no longer simply about reporting. It is becoming an operational infrastructure.

Climate Risk Is Now a Financial Variable

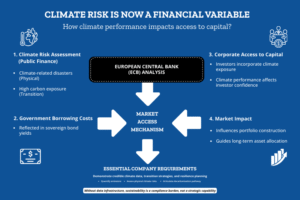

One of the clearest signals comes from the European Central Bank’s recent research examining the relationship between climate risks and sovereign debt markets.

The analysis shows that climate-related disasters and high carbon exposure are increasingly reflected in government borrowing costs. Countries that are more vulnerable to physical climate impacts or more exposed to carbon transition risks may face higher sovereign bond yields over time.

This is not just a public finance issue. It reflects a broader shift in how financial markets assess climate risk.

Investors are increasingly incorporating climate exposure into credit analysis, portfolio construction, and long-term asset allocation. For corporates, this translates into a new reality: climate performance is beginning to influence access to capital.

The transmission mechanism is no longer theoretical; it is embedded in the plumbing of the financial system. The European Central Bank has begun integrating climate risk scores directly into its collateral framework, applying ‘haircuts’ to assets with high carbon exposure or poor transition plans.

Simultaneously, major credit rating agencies are formalising methodologies that downgrade sovereign and corporate ratings based on physical vulnerability. This shifts sustainability from a reputational metric to a direct determinant of borrowing capacity and liquidity access.

In practice, this means that companies must be able to demonstrate credible climate data, transition strategies, and resilience planning. The ability to quantify emissions, assess physical climate risks, and articulate a decarbonisation pathway is becoming essential not just for compliance, but for investor confidence.

Europe’s Industrial Strategy Is Being Rewritten Around Decarbonisation

At the same time, climate policy in Europe is increasingly being implemented through industrial policy rather than solely through environmental regulation.

Recent proposals aimed at strengthening European manufacturing competitiveness increasingly prioritise low-carbon production, local clean-technology supply chains, and green procurement requirements.

Public procurement across Europe represents trillions of euros in annual spending. Governments are now using this purchasing power to favour low-emission materials, cleaner manufacturing processes, and resilient supply chains.

For industries such as steel, chemicals, automotive, and energy infrastructure, this shift is profound. Carbon intensity is quickly becoming a factor not just in regulatory compliance but also in market access.

Companies bidding for contracts or participating in strategic industrial ecosystems must now demonstrate the environmental performance of both their operations and their supply chains.

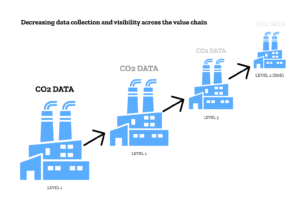

This raises a critical challenge: tracking emissions and sustainability performance across complex global value chains.

However, this demand for granularity creates a critical bottleneck: the SME supply chain. While large corporates possess the capital to build sophisticated data infrastructures, their thousands of SME suppliers often lack the resources and technical expertise to measure and report with similar precision.

This disparity risks fracturing European supply chains, where compliant giants are forced to drop non-compliant local suppliers in favor of less regulated international alternatives. Without targeted support mechanisms to digitize SME reporting, Europe’s push for data transparency could inadvertently undermine its own industrial resilience and competitiveness.

Sustainable Finance Regulation Is Moving Closer to the Investor

Alongside industrial policy, sustainable finance regulation continues to expand across the European Union.

Regulators are now requiring financial advisors to explicitly incorporate investors’ sustainability preferences into investment recommendations. This represents a structural shift in how capital flows are directed.

Rather than sustainability remaining a niche product category, ESG considerations are becoming embedded in mainstream investment processes.

This creates cascading implications across the financial system. Asset managers require reliable ESG data to construct portfolios. Advisors must match products with sustainability preferences. Companies must provide disclosures that enable investors to assess environmental and social performance.

In short, the quality of sustainability data is becoming a determinant of capital allocation.

The Operational Challenge Behind The Policy Momentum

While the policy direction is clear, implementation remains complex.

Many organisations are still grappling with fragmented sustainability data spread across business units, facilities, and suppliers. Scope 3 emissions remain particularly difficult to quantify due to limited supplier data and inconsistent reporting standards.

At the same time, companies must navigate an expanding regulatory landscape that includes frameworks such as the Corporate Sustainability Reporting Directive (CSRD), the EU Taxonomy, and climate-related disclosure standards aligned with international frameworks.

For sustainability leaders, the core challenge is no longer understanding what needs to be reported. The challenge is building the operational systems required to generate reliable, auditable sustainability data at scale.

Without this infrastructure, organisations risk turning sustainability reporting into a manual, resource-intensive exercise rather than a strategic capability.

Sustainability Data As Enterprise Infrastructure

Beyond collection lies the deeper challenge of assurance and data provenance. For sustainability data to function as financial infrastructure, it must withstand the same audit rigor as balance sheets. Yet, a significant portion of current Scope 3 data relies on industry averages and proxy estimates rather than primary source verification.

This creates a ‘garbage in, garbage out’ vulnerability: if the underlying infrastructure is built on estimated rather than verified data, the resulting investment decisions and risk models could face sudden, volatile corrections as actual performance data emerges.

The next frontier is not just gathering data but establishing an immutable chain of custody that satisfies third-party auditors.

As these trends converge, a new reality is emerging. Sustainability data is becoming enterprise infrastructure in much the same way financial reporting systems became essential decades ago.

Organisations increasingly need a centralised data backbone capable of:

- Collecting environmental and operational data across facilities

- Integrating supplier and value-chain information

- Mapping data to multiple regulatory frameworks

- Generating decision-ready analytics for management and investors

When sustainability data is managed effectively, it becomes more than a compliance tool. It enables companies to identify operational efficiencies, manage transition risks, and engage with capital markets more confidently.

The Infrastructure Imperative

As these trends converge, it becomes evident that sustainability data is no longer merely a compliance exercise, but rather a fundamental component of the European financial infrastructure. However, building this foundation requires more than software.

It demands a resolution of the SME capacity gap, a rigorous shift from proxy estimates to audited primary data, and a move toward real-time verification.

Companies that treat this transition as a strategic overhaul (integrating climate intelligence directly into treasury, procurement, and risk functions) will secure lower capital costs and preferential market access. Those that view it merely as a reporting obligation, risk finding their data deemed unreliable, their supply chains fragmented, and their cost of capital increasingly penalised.

The transition is no longer about transparency. It is about building an operational backbone capable of withstanding the scrutiny of a decarbonising economy.