Financial institutions are no longer just financial intermediaries; they have become key players in shaping climate outcomes globally. One of the most important concepts for banks and asset managers today is financed emissions; the greenhouse-gas emissions associated with companies they lend to or invest in. Understanding and managing these emissions is rapidly becoming essential for climate risk management, strategy, and reporting.

What Are Financed Emissions and Why They Matter?

“Financed emissions” are emissions generated by the activities of organisations that a financial institution lends to, invests in, or underwrites. In other words, a bank’s or asset manager’s indirect carbon footprint through its financing and investment portfolio. These emissions fall under Scope 3 (category 15) of the Greenhouse-Gas Protocol, which covers “investments” (including loans, equity, bonds) of financial institutions.

Why the growing focus? Because for many banks the emissions tied to their portfolios are orders of magnitude larger than their own operational emissions — meaning that most of their climate footprint, and hence climate risk, sits outside their direct business. ibm.com

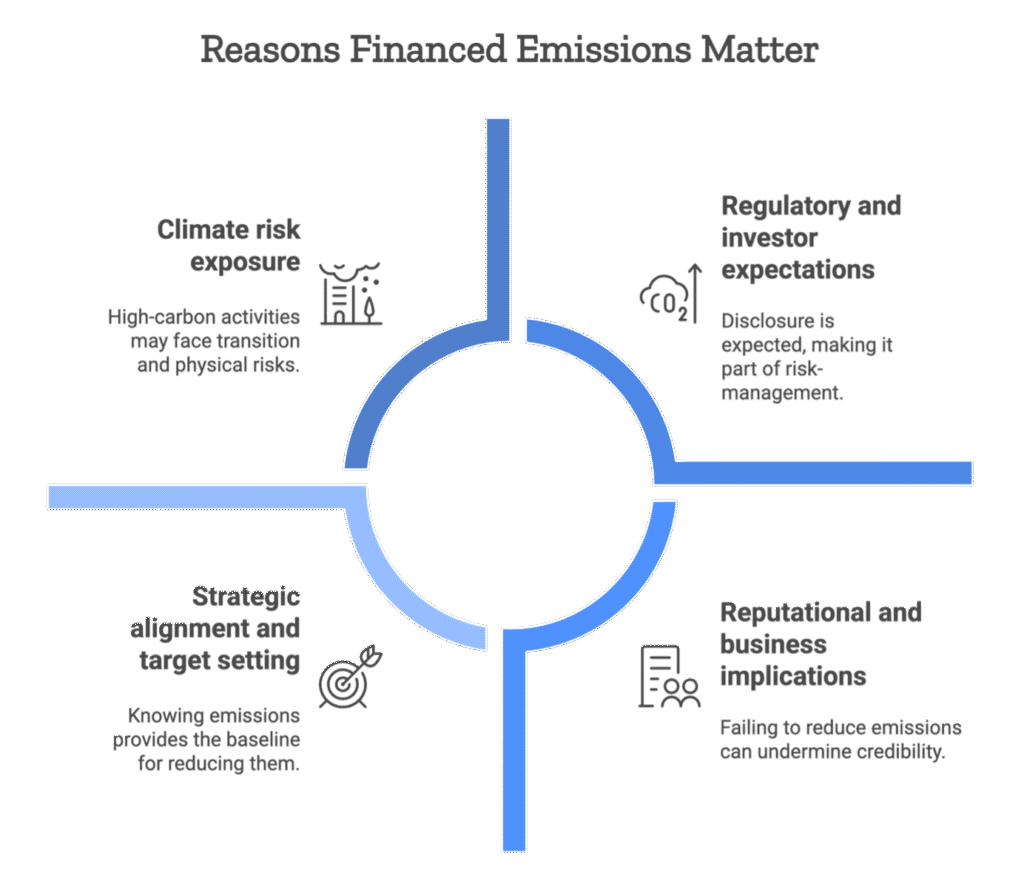

Financed emissions matter for several reasons:

- Climate risk exposure: A portfolio weighted toward high-carbon activities may face transition risks (policy changes, carbon pricing, stranded assets) and physical risks (impacts from extreme weather). By measuring financed emissions, institutions gain insight into where they stand.

- Regulatory and investor expectations: Finance regulators, investors and global frameworks increasingly expect disclosure of financed emissions, making them a part of risk-management and disclosure regimes.

- Strategic alignment and target setting: You cannot steer what you do not measure. Knowing your financed emissions provides the baseline for reducing them and aligning portfolios with climate goals (e.g., limiting warming to 1.5 °C).

Reputational and business implications: As stakeholders demand transparency and alignment with climate goals, failing to account for and reduce financed emissions can undermine credibility or competitiveness.

In short, financed emissions are central to how financial institutions view their role in, and exposure to, the low-carbon transition.

The SBTi for Financial Institutions: Targeting Portfolio Emissions

The Science Based Targets initiative (SBTi) is a leading global initiative that helps organisations set greenhouse-gas (GHG) reduction targets consistent with limiting global warming. For financial institutions, SBTi has tailored guidance that recognises that the largest emissions lie in lending and investment portfolios.

Key features of SBTi’s financial-institution work:

- The Financial Institutions Near-Term Criteria and the newer Financial Institutions Net-Zero Standard enable banks and asset managers to commit to science-based targets for their financed emissions.

- Targets must cover significant portions of the portfolio (lending, investing, underwriting) and align with pathways that limit warming to 1.5 °C or well below 2 °C.

- Institutions are expected to phase out or reduce high-carbon financing and align new business with low-carbon trajectories.

- The key to success is credible measurement (i.e., financed emissions data) combined with strategy and alignment; hence, SBTi and measurement frameworks tie together.

In effect, SBTi gives banks and asset managers a destination and roadmap, a science-based pathway for reducing the emissions associated with what they finance. However, setting targets is only meaningful if measurement and reporting are robust, which brings us to PCAF.

PCAF: Measuring Financed Emissions Consistently

Measurement of financed emissions is complex: different asset classes, uneven data, and attribution challenges. The Partnership for Carbon Accounting Financials (PCAF) was created to help financial institutions measure and disclose those emissions in a standardised way. carbonaccountingfinancials.com

Some key points about PCAF:

- Its Global GHG Accounting & Reporting Standard for the Financial Industry provides methodologies for attributing emissions from key asset classes (equity, bonds, business loans, real estate, etc.).

- It enables institutions to calculate, attribute and report financed emissions in a comparable way, which is critical for transparency and benchmarking.

- PCAF and SBTi are complementary: PCAF provides the measurement system; SBTi provides the target-setting framework.

- In recent years, hundreds of financial institutions globally have committed to or used PCAF methodologies.

For banks and managers, adopting PCAF means establishing a credible baseline of financed emissions, increasing data quality over time, and producing disclosures that meet stakeholder expectations. In turn, that enables alignment with SBTi commitments.

Moving from Metrics to Action: Risk, Alignment & Disclosure

When banks and asset managers measure financed emissions and commit to science-based targets, several interlinked impacts emerge in their strategy and operations:

Risk Assessment

Measurement enables identification of carbon-intensive exposures. Once quantified, institutions can run scenario analyses (e.g., warming pathways, carbon pricing) to test how portfolios might behave under transition or physical risk. This elevates climate risk from a qualitative concern to a quantifiable input into credit risk, investment decisions and stress testing.

Portfolio Alignment

With baseline data and targets, institutions are able to steer capital toward lower-carbon assets, reduce or exit high-carbon exposures, and engage clients/investees on transition plans. For example, financed emissions scoring may become part of credit approval processes or portfolio construction criteria.

Disclosure & Transparency

Stakeholders now expect disclosure of financed emissions, reduction targets, and progress. Frameworks such as the International Sustainability Standards Board (ISSB) and regional regulation increasingly require this. Reliable measurement (via PCAF) and credible targets (via SBTi) enhance transparency and trust, and support comparability across institutions.

Together, these elements fundamentally shift how financial institutions operate — climate risk is no longer a niche consideration; it is integrated into core business strategy, portfolio design, governance and disclosure.

Strategic & Reporting Implications for Financial Institutions

For banks and asset managers, the implications of this shift are significant:

- Strategy: Climate must be embedded into business strategy. Institutions may need to reassess sector exposures, client relationships and product offerings. Growth may be driven more by low-carbon financing than traditional high-carbon business.

- Risk Management: Credit, investment and underwriting decisions increasingly include climate criteria. Governance structures must account for climate risk at the board level and across business functions.

- Data & Reporting Capabilities: Reliable measurement of financed emissions demands new data capacities, analytics, and disclosure workflows. Over time, climate metrics are becoming as material as financial ones.

- Competitive Positioning & Reputation: Institutions that can demonstrate clear financed-emissions reductions, credible targets and transparent disclosures can attract capital, clients and talent. Conversely, lagging institutions may face regulatory, investor or reputational challenges.

- Capital Allocation: The reallocation of finance toward low-carbon, climate-resilient activities becomes a practical business objective, not just a sustainability goal.

In effect, financed emissions become a bridge between the traditional financial paradigm and the emerging climate-aligned economy.

Conclusion

Financed emissions have moved from the periphery of sustainability reports into the heart of how banks and asset managers assess risk, allocate capital and report to stakeholders. Frameworks like SBTi and PCAF provide the tools to measure where you are, commit to where you want to be, and disclose how you’re getting there.

At Credibl, we understand that navigating this evolution is challenging — from data collection and portfolio measurement to target-setting and assurance-ready disclosures. Our AI-powered ESG platform supports financial institutions with financed emissions tracking, portfolio alignment analytics and integrated disclosure workflows, reducing complexity and increasing confidence in climate-aligned finance.

Start building your climate-resilient finance foundation today with Credibl.

Book a demo to see how you can operationalise financed-emissions measurement, set science-based targets and step into the new era of climate-aware finance.

Frequently Asked Questions (FAQs)

Q1: What exactly counts as financed emissions?

A1: Financed emissions are the greenhouse-gas emissions generated by activities financed by a financial institution, such as loans, equity investments, bonds or underwriting. They represent the indirect “portfolio” emissions of banks and asset managers (Scope 3, category 15).

Q2: Why should financial institutions care about financed emissions?

A2: Because financed emissions provide visibility into an institution’s exposure to climate risks, enable alignment with low-carbon pathways, and increasingly determine regulatory, investor and stakeholder credibility.

Q3: How do SBTi and PCAF differ, and how do they work together?

A3: PCAF focuses on measurement — providing methodologies to calculate financed emissions. SBTi focuses on target-setting — helping institutions commit to science-based reductions in those emissions. Together, they enable a measurement-to-management loop.

Q4: Does measuring financed emissions require perfect data from investees/borrowers?

A4: No — data gaps are common. Frameworks like PCAF include methods and proxy approaches for estimation. Institutional measurement should aim for improvement over time while being transparent about assumptions.

Q5: Is reporting financed emissions mandatory?

A5: It depends on jurisdiction. Some regulations already require disclosure of portfolio-level emissions. Global frameworks like ISSB and EU-ESRS are moving toward formalising these requirements.

Q6: What role does financed emissions play in risk modelling?

A6: Financed emissions serve as a key input for scenario analysis, stress testing and risk assessment of portfolios under transition or physical-climate pathways. They help identify high-carbon exposure and inform capital allocation, pricing and governance decisions.